How To Protect Your Home From Medicaid Liens

How to Protect Your Home from Medicaid Liens

Roughly 70% of adults over age 65 will need some form of long-term care in their lifetimes. But the average private room in a nursing home costs over $10,000 per month in Rhode Island. So, many people may need assistance from Medicaid to get the care they need. But Medicaid will liquidate all your assets before they start to pay, so how do you protect your home from Medicaid?

Medicaid can try to recoup their financial losses after a Medicaid beneficiary dies. In many cases, that includes putting a lien on their house. This could end up forcing the sale of a person’s home after their death, leaving their beneficiaries with nothing.

But, you don’t necessarily need to sacrifice your home to become a Medicaid beneficiary. With planning and help from a Rhode Island estate planning lawyer, you can protect your home from the Medicaid estate recovery program. Find some of the most common methods to protect property and assets from Medicaid below.

What Is The Medicaid Estate Recovery Program?

Think of Medicaid as a type of interest-free loan. A person who qualifies for Medicaid can benefit from financial assistance during their lifetime. But at the time of that person’s death, Medicaid will attempt to recover the money from the person’s estate when their assets fall into probate. It’s a process called Medicaid estate recovery.

Medicaid estate recovery applies to people who:

● Started receiving Medicaid benefits at age 55 or older.

● Were permanently institutionalized at any age

● Didn’t have a surviving spouse or other dependents deemed to have a deserving claim on the estate.

Can Medicaid put a lien on your House?

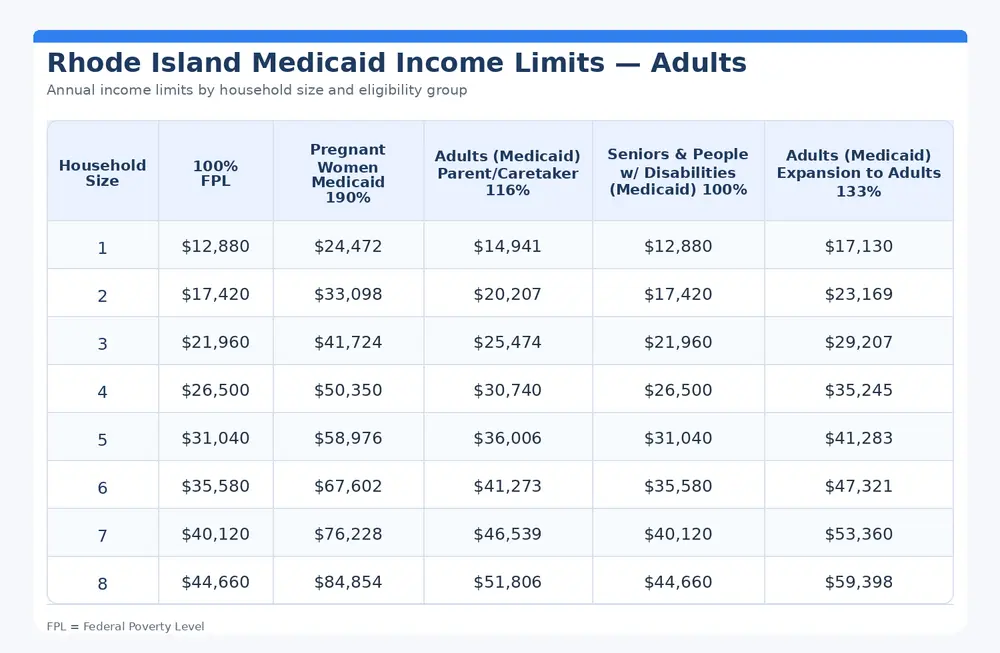

In Rhode Island, a person must have $4,000 in total assets or less to qualify for Medicaid. But a person’s primary residence doesn’t count toward this total if the total equity is $688,000 or less and the person intends to return to their home after treatment.

However, if the Medicaid beneficiary dies and their house falls into probate, Medicaid has the ability to place a lien on their home as part of estate recovery. Medicaid can also place a lien on a person’s home while they’re still alive. But they can’t sell it until after the person has died.

Can Medicaid Take a Jointly Owned Home?

Medicaid can’t take a deceased person’s home if they have a living spouse that still resides in the house. However, they can still put a lien on the house and sell it at the time of the spouse’s death.

Beyond a living spouse, Medicaid also can’t take possession of a house if any of the following people still reside there.

● A child under the age of 21.

● A child of any age that’s blind or disabled.

● A sibling with an equity interest in the home. They must have lived in the home for at least one year before the Medicaid beneficiary entered a nursing home.

Do Medicaid Liens Expire?

Medicaid can put a lien on a person’s house while they’re still alive. However, if the Medicaid beneficiary leaves a nursing home and returns to their house, then the state has to release the lien.

How Can You Protect Your Home & Assets from Medicaid?

Gifting

One of the simplest ways to prevent Medicaid from placing a lien on your house is to sell or gift it to someone else. This keeps your home from falling into probate at the time of your death, since another person will already legally own it.

However, this needs to be done well in advance. Otherwise, it will violate the five-year Medicaid lookback period. The recipient will also need to pay gift taxes which could make other options a more practical choice.

Irrevocable trusts

In some cases, transferring your home to an irrevocable trust could shield it from Medicaid estate collection. Putting your home in a trust means that it isn’t technically a part of your estate anymore. Instead, it belongs to the trust and will help your home avoid falling into probate.

That said, an irrevocable trust needs to be set up well in advance to prevent violating the Medicaid 5 year lookback period. So, you may need an estate planning attorney’s guidance to set up the trust properly.

Life estate

In some cases, a “life estate without powers” might be a viable option. This essentially allows you to give one or more people ownership interest in your property.

The original owner is called the “life tenant,” and has full legal control over the property during their lifetime. At the time of the life tenant’s death, the property will automatically pass to the remainderman — the other person involved in the life estate. Since the home transfers automatically, it will not fall into probate and can help shield it from Medicaid.

Caregiver child exemption

A rule called the “caregiver child exemption” allows an elderly person to transfer their home to an adult child who acted as their caretaker. This exemption is meant to provide a form of compensation for adult children who are able to keep their aging parents out of a nursing home.

To qualify for this exemption, the caregiver child has to live in their parent’s home for at least two years prior to the parent being admitted to a nursing home or assisted living facility. The child should have also provided a level of care that prevented their senior from needing to transfer to an elder care facility.

Then, after the elderly parent dies, Medicaid can’t enforce a lien on the home as long as the caregiver child still resides there.

Conclusion

Medicaid rules and regulations can be difficult to understand, so don’t put off Medicaid planning until it’s too late. Start protecting your home today with help from Warwick RI lawyer Brian Nappa.

As an experienced estate planning attorney, Bryan Nappa understands the nuances of Rhode Island’s Medicaid laws, and he can help guide you toward the best estate planning solution for your unique situation. You can protect your assets for your beneficiaries and find peace of mind as you plan for the future. Contact his office today to learn more about Medicaid estate planning and how to protect assets from Medicaid.